The

Federal Hearing

and Anti-Militarism Walk

• March

5, 1999 •

| In Brief: Most of the 20-minute hearing was spent by the judge persistently grilling the U.S. attorney with questions regarding the Fifth amendment. In the end, the judge asked Hedemann to go once again to the IRS office and assert the Fifth question-by-question rather than in a "blanket" manner. The judge hinted that the IRS might want to drop the whole matter after that, fully expecting Ed to assert the Fifth for everything except his name and address. As an aside, the U.S. attorney raised the specter of the IRS granting Ed immunity [thus removing the Fifth as a reason not to turn over documents]. |

Anti-Militarism

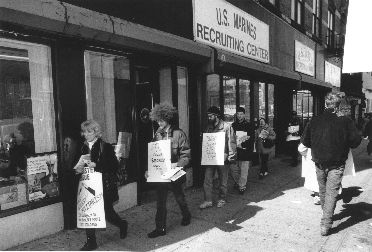

Walk Through Brooklyn

About 20 to 25 of us gathered

at 11 am on March 5, 1999, in front of the military recruiting

offices in downtown Brooklyn to picket and leaflet. The recruiters

were mildly amused by the activity. After a half hour, we began the mile-walk

(see map) to Federal Courthouse, first with

a 20-minute stop at the IRS building for more picketing

and leafleting before continuing our walk through the downtown shopping

area of Brooklyn. While at the IRS, a couple groups of young school children

came by, very curious about what we were doing. The teacher of one group

stopped to explain to the kids what the issues were, then he even joined

us in chanting "We are not willing to pay for killing."

|

|

Picket

and leafleting outside the military recruiters |

.

. . in front of Brooklyn IRS building |

We reached the Federal Courthouse at about 12:30 after

passing out about 1000 WRL

tax pie charts and 1000 leaflets printed for the occasion.

We paused just outside to gather as a group, hung our signs on the plywood

fence surrounding an adjoining construction site. This attracted the

attention of Federal guards inside who came out to find out what was

going on and ask us to remove the signs. As we filed into the courthouse

it was clear that we had been expected. More than the usual complement

of guards were on duty to process us through the metal detectors and

scanners. A couple of guards, thinking they were out of earshot, discussed

whether it was possible to keep the "protesters from coming inside"

but decided that we had a "constitutional" right to go in.

We were allowed to place our signs in corner just inside the entrance

such that we could retrieve them later.

The

Federal Hearing

As we reached the courtroom on the

top floor, we were told that the front two rows (out of 10) were for

the U.S. Marshals. There appeared to be about 10 of them (for "regular" cases

there might not be any marshals). About 50 of us were on hand for the

half hour we were in the courtroom. It seems they were preparing for

protests or possible disruption of court decorum.

The U.S. attorney showed up just before the 1 pm scheduled start of

the hearing. The judge entered the courtroom a few minutes later, but

without the formal announced "all rise." Many of us remained

seated not in disrespect to the judge but in the belief that all people

are equal--neither above or below anyone else. After asking Hedemann

and U.S. attorney Levy to approach the bench, Judge Amon immediately

launched into a persistent questioning of Levy about the Fifth amendment.

Most of the 20-minute hearing was question-response between the judge

and U.S. attorney. The judge was clearly not satisfied by the government's

position on the Fifth and what would be gained by having Ed return

to the IRS only to respond with the Fifth item-by-item to each IRS

question.

Among the Judge's

Questions: What exactly does the government expect

her (the judge) to order Hedemann to do--go to the IRS office again?

Answer the questions item by item? Produce documents? Wouldn't that

process be incriminating? How does the IRS determine what's proper

to claim the Fifth on and what isn't?

Among the U.S. Attorney's Responses: The IRS has many levels

in their process to evaluate what's an appropriate use of the Fifth. Because

she doesn't work there she doesn't know all those processes. The IRS will determine

whether it will grant immunity.

Then the judge turned to Ed to ask if he could meet once again with the IRS and assert the Fifth item-by-item where he wanted. It seems she wants to allow the IRS this procedural step and then if the case returns to court she will decide if the IRS has come up with any more substantial arguments regarding why the Fifth amendment would not apply. Ed agreed to thism and with U.S. Attorney Levy set March 8, 1999, as the date to meet with the IRS.

Witness Fees. At

this point the judge appeared ready to end the hearing when Ed raised

the issue of witness fees. [The IRS owes $40 for each summons appearance

as a witness fee; something that few people are aware of and if it

became better known, in the view of some observers, might discourage

indiscriminate issuing of summonses by the government. The government's

position: no witness fees were owed since Ed didn't answer the IRS's

questions.] The judge asked the U.S. attorney about this, and she responded

that he has to answer questions first and that if the fee were granted it

would be taken out of money he owes the IRS. The judge wanted

to see paperwork on that and indicated that she would rule on the witness

fee issue later.

Political and Moral Issues. Again as the judge appeared to

want to wrap up the proceedings, Ed raised the "military spending" and

his having

"already paid the taxes" issues that he had in his January 21, 1999,

written brief, which were dismissed by the government in its March 1, 1999,

written response. The judge said that the Fifth amendment was the only issue

she felt was appropriate for this summons enforcement hearing and would not

deal with the other issues. She said they might be appropriate in a criminal

proceeding but not now. At that point the hearing was ended.

During the milling around in the courtroom as we got up to leave, Ed

announced that we should gather outside the courthouse for a group photo.

He invited the marshals and other court officials to join us. They demurred

(but found it all quite amusing).

|

After the hearing on March 5, 1999. |

Last updated 3/12/99

return to U.S. v. Hedemann page